The energy debate was polarised long before Russia’s invasion of Ukraine. Those divisions are being cleaved wider with every day that passes. There is a popular take doing the rounds among a certain faction of energy commentators that goes like this:

Europe tried to rely on renewables but moved too fast, leaving itself reliant on natural gas for backup – which it naively procured from Russia, strengthening the hand of Vladimir Putin and funding Russian military expansionism. Therefore, green policies and decarbonisation bear some responsibility for the atrocities we are now witnessing in Ukraine.

Go deeper with GlobalData

There is a lot to unpack here, but let’s get one thing clear: responsibility for Russia’s military atrocities in Ukraine lies with Vladimir Putin. Energy policies drawn up by the European Commission and EU member states cannot be conflated with Moscow’s malevolent military manoeuvres.

That is not to say mistakes weren’t made. Putin has for years been allowed to consolidate Russian influence in Europe, and cheap energy is the most powerful tool in Moscow’s foreign policy armoury. ‘Sticky’ demand for Russian oil and natural gas, particularly in transport and domestic and industrial heat, respectively, gifted the Kremlin great leverage over European affairs.

Europe’s dependence on Russian gas was short-sighted. A fateful mix of naivety towards Russia’s trustworthiness, prioritisation of ‘the market’ over geostrategic allegiances, wilful historical ignorance and corruption of European energy politics all created opportunities for Moscow to exploit.

Russia apologists should apologise

These mistakes are particularly prevalent in Germany, where an uneasy political closeness with Russia paved the way for the construction of the Nord Stream 1 and 2 pipelines. A naïve belief in Russia as a rational market actor also greased the wheels in Germany’s shift from nuclear to gas-fired power.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataIt is notable that Germany is among the staunchest opponents of EU sanctions on Russian oil and gas exports. Ex-Chancellor Gerhard Schröder, who sits on the boards of sanctioned Russian state oil and gas giants Rosneft and Gazprom, has spent much of his time since leaving office furthering Russia’s energy interests in Germany. Schröder refuses to criticise his close friend Putin over Russia’s actions in Ukraine, and is now playing the unlikely role of peace broker.

Schröder and other Russian apologists bear some responsibility for the EU’s failure to diversify its gas supplies despite the many warning signs over the years. The ‘gas wars’ of the 2000s – which saw sporadic interruptions in Russian gas flows into former Soviet states and eastern and southern Europe – gave rise to the Southern Gas Corridor, an immense 3,500km pipeline network from Azerbaijan to Italy designed to diversify European gas supplies.

Yet dependence on Russian gas has actually increased since the diversification policy was first adopted. Russia’s share of EU gas imports rose from 30.6% in 2010 to 33.3% in 2014, when Russia annexed Crimea, and continued rising thereafter to 38.2% in 2020 at the expense of nearly every other gas-exporting country:

This is why Europe today finds itself bankrolling Russia’s military. European countries buy 49% of Russia’s 4.7 million barrels per day of oil exports, 74% of its 8.9 trillion cubic feet per year of natural gas exports, and 32% of its 262 million tonnes per year of coal exports.

A tragic irony is that this war is adding a stratospheric risk premium to Russian energy exports, borne by consumers. In 2020, Europe paid Russia €8bn for gas, €32bn for crude oil and €15bn for oil products. With war and sanctions adding fuel to already-overheated global oil and gas markets, that figure will probably be much larger in 2022.

Time for renewables 2.0

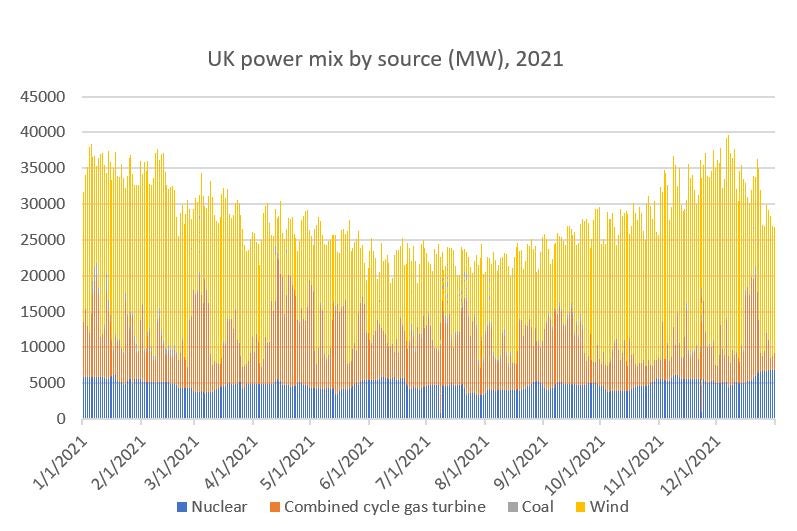

Anti-renewables zealots have been quick to accuse variable-output power generators for exacerbating the EU’s Russian gas dependency. ‘Dunkelflaute’ – a German word describing lengthy mid-winter periods of low wind and solar availability coinciding with high heat and electricity demand – is often cited as the Achilles’ heel in Europe’s embrace of intermittent energy sources.

It is true that energy storage technologies cannot yet displace gas in its role of covering prolonged or seasonal variations in renewable output, but that is not to say renewables aren’t helping. On the contrary, wind and solar displace power generation from other sources, and since they have no fuel costs, they displace more expensive conventional generation, such as thermal power from gas, coal or other fossil fuels.

If Europe had installed zero wind turbines and solar panels, what would its electricity mix look like today? Nuclear would not necessarily have risen to the challenge. For a variety of reasons, the European nuclear industry ran out of steam long before wind and solar became mainstream. The electricity sector would be even more dominated by gas and coal, not less.

Gas will for some time remain the best option for ramping up and down to balance renewables at scale. Every kilowatt-hour of wind or solar power replaces a kilowatt-hour of gas. Now, does this add wider system balancing costs? Absolutely. Hence the introduction of capacity markets to remunerate dispatchable plants for their availability and reduced running hours.

The cost of these schemes should be considered holistically as part of the renewables pivot. ‘Naked’ wind and solar projects – those not integrated with energy storage or another balancing component – have been great for investors, which garner part of their profits by socialising these costs.

However, the UK and Europe need to move on from that failed model. A good first step would be for governments and clean energy advocates to go beyond misleading references to the ‘falling’ levelised cost of energy (LCoE) of wind and solar when defending decarbonisation policies, because LCoE does not account for the rising costs of renewables integration.

Intermittency and security of gas supply are two sides of the same coin and demand a single unified policy response that considers system-wide impacts. Wind and solar present challenges to the design of secure, reliable and efficient electricity markets, but these are not insurmountable, and these power sources should not be discarded as mainstay options in the energy transition. They deserve an adequate and honest assessment of their inherent costs and benefits beyond the myopic confines of LCoE.

Structural dependency

Another EU failure can be identified in market design. Liberalisation of EU energy markets led to market-based pricing of electricity, which incentivised the dispatch of the most economic generators at any given moment.

It may be hard to imagine today, but gas was cheap and abundant in much of Europe for many years thanks to strong domestic production from the North Sea and conventional onshore fields. This favoured investment in gas-fired power generators, which have much lower upfront construction costs than coal, nuclear, wind and solar plants.

Implementing a power market that favours natural gas created a structural exposure to wholesale gas prices. As the EU’s domestic production base dwindled and imports rose, this translated into exposure to global gas prices – placing an ever-greater emphasis on the need to source the cheapest gas from foreign suppliers.

The biggest driver of European gas import dependency has thus been waning domestic production. This is a function of reservoir depletion in mature hydrocarbon provinces such as the North Sea, lacklustre exploration results in frontier provinces such as the Barents Sea and the failure to find unconventional shale gas resources.

Scant viable alternatives

Even those European countries that tried hardest to unlock commercial volumes of shale – Poland, for example – failed in their attempts. Hopes of emulating the US shale revolution in Europe were waning well before fracking bans and moratoria put an end to exploratory drilling.

Buying Russian gas was therefore pragmatic. The sheer volume, affordability and availability was a boon for consumers. No other source ever came close, and that holds true today. Liquefied natural gas (LNG) could never have scaled quickly enough to replace Russian volumes, and it cannot do so now.

In 2020, Europe imported 167.7 billion cubic metres (bcm) of pipeline gas from Russia, according to BP. Europe’s LNG imports were 114.8bcm that year, which represents a 24% share of global LNG trade in 2020 (487.9bcm).

Even if Europe were to somehow more than double its LNG procurement to replace lost Russian piped gas (and deprive Asian consumers of these same volumes), this amount of LNG cannot be easily injected into the EU gas grid. EU 27 regasification capacity currently stands at 156bcm, and expanding this in southern and eastern Europe, where it is needed most, would take years. The EU imported record amounts of LNG in January 2022, and quickly ran up against capacity constraints.

Flexibility = fickle flows

Should European gas buyers pay a ‘security premium’ to procure more expensive gas from allies, such as LNG from the US? European offtakers pretty much bankrolled the first wave of US liquefaction projects, but the flexibility of those contracts allowed much of it to flow to premium Asian markets.

Should EU buyers insist on destination clauses to ensure LNG cargoes arrived at European terminals? That would have gone against US commercial practice, which introduced flexible cargoes delivered on the water on a ‘free on-board’ (FOB) basis.

The buyer of an FOB cargo must pay for shipping costs, but in return gets complete freedom to redirect the product to the most profitable destination. This is what made US LNG so attractive to European buyers in the first place: the ability to exploit global arbitrage opportunities.

[Keep up with Energy Monitor: Subscribe to our weekly newsletter]

Restricting US LNG destination flexibility would also contravene EU competition rules. The Commission launched an anti-trust investigation into Qatar Petroleum in 2018 over its restrictive long-term contracts. This process was recently dropped because, ironically, Europe now really needs any LNG the Qataris can spare.

Undoing rules that underpinned the EU single market would have tempered the deregulatory push in the 2010s to transition away from oil indexation and embrace market-based gas hub pricing. This shift saved EU consumers an estimated $70bn (€63.75bn) over the past decade by exposing Gazprom to competition from global suppliers (that is to say, LNG) and holding its feet to the fire in price negotiations.

Liberalisation and complacency

This worked fairly well for many benign years until, of course, markets tightened. The lesson here is that outsourcing energy security to ‘the market’ means paying market rates to compete for marginal supply. It means consumers benefit more during a global glut, and suffer more when there is a shortage.

Should European policymakers have predicted that Gazprom would exploit this vulnerability to manipulate European markets and further Russia’s influence? Probably, although that is a geostrategic political question that goes beyond the remit of those tasked with designing efficient energy markets.

If anything, insufficient attention was given to the security implications of relying on cheap Russian molecules in an energy system designed to favour short-run marginal costs over all other considerations. Put it down to a lack of joined-up thinking, deliberate complacency or a mix of the above – but don’t blame renewables.