Climate change is causing sea levels to rise faster than for 3,000 years, bringing a “torrent of trouble” to almost a billion people, UN secretary-general António Guterres told the UN Security Council on 14 February. “Low-lying communities and entire countries could disappear forever. We would witness a mass exodus of entire populations on a biblical scale.”

One country in the firing line is Cape Verde. The West African island nation, where 80% of the population lives on the coast, is already feeling the brunt of rising sea levels and increasing ocean acidity on its infrastructure, tourism, biodiversity and fisheries. The country desperately needs to both mitigate and adapt to these problems, but – as with many Global South countries at present – simply lacks the budget to do it: Cape Verde’s debt reached an all-time high of 157% of GDP in 2021.

Go deeper with GlobalData

In a bid to address both issues simultaneously, the country has signed a novel agreement with Portugal to swap some of its debt for investments into an environmental and climate fund. The former Portuguese colony owes the Portuguese state €140m ($148m) and Portuguese banks €400m.

On a state visit to Cape Verde on 23 January, Portuguese Prime Minister António Costa announced the debt would be put towards Cape Verde’s energy transition and fight against climate change. Costa earmarked projects involving energy efficiency, renewable energy and green hydrogen as possible targets for the fund.

“This is a new seed that we sow in our future cooperation,” said Costa. “Climate change is a challenge that takes place on a global scale and no country will be sustainable if all countries are not sustainable.”

“Debt-for-climate swaps” allow countries to reduce their debt obligations in exchange for a commitment to finance domestic climate and nature projects with the freed-up financial resources. The concept has been knocking about since the 1980s, typically geared at nature conservation. However, after recent deals for Barbados, Belize and the Seychelles, and huge $800m and $1bn agreements in the offing for Ecuador and Sri Lanka, is this financial instrument finally coming of age?

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataA triple threat

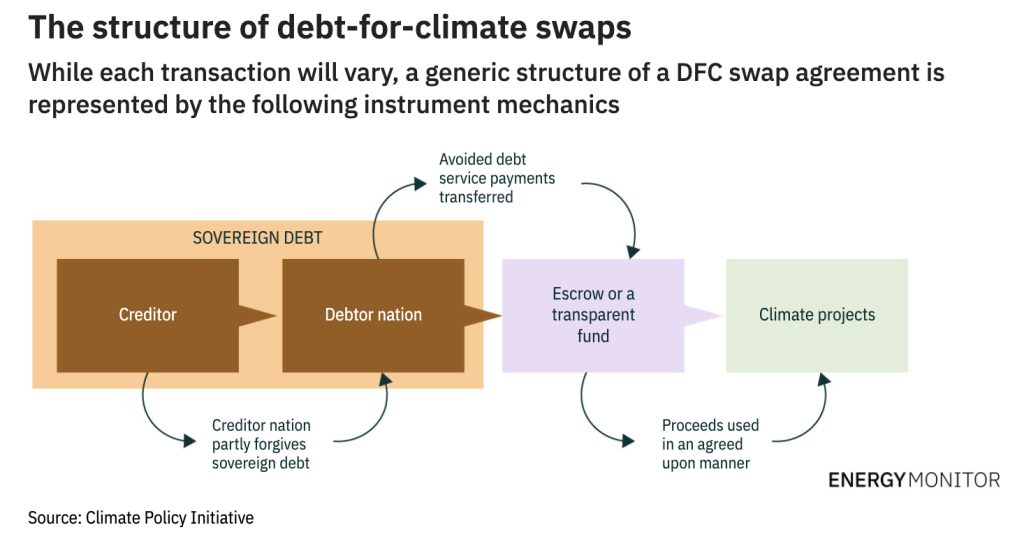

Debt-for-climate swaps typically follow a formula. First, a creditor agrees to reduce debt, either by converting it into local currency, lowering the interest rate, writing off some of the debt, or a combination of all three. The debtor will then use the saved money for initiatives aimed at increasing climate resilience, lowering greenhouse gas emissions or protecting biodiversity.

The original 'debt-for-nature swaps' began as small, trilateral deals, with NGOs buying sovereign debt owed to commercial banks to redirect payments towards nature projects. They have since evolved into larger, bilateral deals between creditors and debtors. Today’s debt-for-climate swaps (or 'debt-for-environment swaps' or 'debt-for-climate-and-nature swaps', depending on who you ask) are much larger in scale and are programme rather than project-based, with delivery and budget accountability resting with the host governments, not international NGOs.

Debt-for-climate swaps free up fiscal resources so governments can improve resilience and transition to a low-carbon economy without causing a fiscal crisis or sacrificing spending on other development priorities. The instrument can create additional revenue for countries with valuable biodiversity or carbon sinks by allowing them to charge others to protect those assets, thereby providing a global public good. Swaps can even result in an upgrade to a country’s sovereign credit rating, as was the case in Belize, which makes government borrowing cheaper.

Right now, these instruments are needed more than ever, with low-income countries dealing with multiple crises that have put huge pressure on public debt. “There is massive debt distress: Sri Lanka’s defaulted, Ghana’s on the brink, as is Zambia and Chad,” says Paul Steele, chief economist at the International Institute for Environment and Development (IIED). “It was bad going into the pandemic, but the pandemic made it a lot worse because these economies collapsed, and they had to borrow lots of money from the IMF and World Bank. Then it got even worse after the Ukraine crisis because energy and food prices went through the roof.”

About 60% of low-income developing countries are already at high risk of, or are currently in, debt distress. “Many of these countries face a triple whammy; they are often most vulnerable to climate change impacts, and for some, have a high dependence on fossil fuels,” says Nicola Ranger, senior researcher at Oxford’s Smith School of Enterprise and the Environment.

A total of 63 countries could see debt downgrades due to climate change, making it even harder to finance debt. It becomes increasingly difficult for them to finance the investments needed in climate adaptation and low-carbon development. “Debt-for-climate swaps can help countries escape this triple threat and make the investments they need to make in low-carbon, climate-resilient development,” says Ranger.

There is also, of course, the looming urgency of the environmental crisis. Estimates from the Paulson Institute, a think tank, find that to reverse the global decline in biodiversity by 2030, countries need to spend between $722bn and $967bn each year over the next ten years. Taking into account what is being spent currently, that puts the biodiversity financing gap at an average of $711bn per year.

In addition, the Climate Policy Initiative (CPI) estimates that, although climate finance flows have almost doubled to more than $650bn over the past decade, that amount needs to increase by at least 590% to $4.35trn annually by 2030 to meet global climate objectives.

“The levels of climate finance are woefully inadequate at present, and we need as many of these kinds of financial instruments as we can deploy,” says Vikram Widge, senior advisor for climate finance at CPI.

Debt-for-climate swaps: “Increasing in size and scale”

Although debt-for-climate swaps are not new, until recently the amount of finance raised globally from the instrument has been modest – just $1bn between 1987 and 2003, according to one OECD study. Just three of the 140 swaps over the past 35 years have had a value of more than $250m, according to the African Development Bank. The average size was a mere $26.6m.

However, the market has steadily picked up pace over the past two decades, adding another $2.7bn of transactions, and some are now forecasting the market will grow as large as $800bn. In 2016, the government of the Seychelles signed a landmark agreement with developed nation creditor group the Paris Club, supported by NGO The Nature Conservancy (TNC), for a $22m investment in marine conservation. The government of Belize followed suit in 2021 by issuing a $364m blue bond – a debt instrument to finance marine and ocean-focused sustainability projects – to buy back $550m of commercial debt to use for marine conservation and debt sustainability. Then, last year, Barbados completed a $150m transaction, supported by the TNC and the Inter-American Development Bank, allowing the country to reduce its borrowing costs and use savings to finance marine conservation.

“Two or three years ago, we were talking about $50m deals,” says Widge. “Now they have gone to $250–300m, so they are definitely increasing in size and scale.”

[Keep up with Energy Monitor: Subscribe to our weekly newsletter]

Indeed, the success of the deals for the Seychelles, Belize and Barbados, along with the debt distress sweeping across the Global South, has sparked an uptick of interest in the model. Ecuador is reported to be in negotiations with banks and a non-profit for an $800m deal, and Sri Lanka is discussing a $1bn transaction – which would be the biggest swap to date.

In reality, debt-for-climate swaps are just one of a number of new sovereign sustainable financing mechanisms being advanced. Other forms of financing appear to be taking off quicker, particularly sustainability-linked sovereign bonds (SLBs) such as those recently issued by Uruguay and Chile, and green bonds. SLBs are performance-linked bonds that reward the issuer for achieving sustainability goals, helping mobilise more private investment into sustainability. “But [green bonds and SLBs are] not a viable solution for countries in debt distress,” says Ranger. “And various facilities are coming into play to support the most vulnerable countries to develop debt-for-climate swaps.”

Rough around the edges

Debt-for-climate swaps are not without their problems, however. The instrument still struggles with complex governance and the ability to mobilise enough finance to make a meaningful dent in public debt to liberate funds for mitigation and adaptation.

Debt swaps are not built into the international financial architecture, so transaction costs for individual swaps are typically high. Plus, for many credit rating agencies, a debt swap technically counts as a default, so it would negatively impact the credit rating of the country. “The ratings agencies really need to change that,” says Sejal Patel, a researcher at the IIED.

Creditors are also not very supportive yet, which impedes the market scaling up, and the transactions need to be large enough to actually provide some debt relief as well as the investment in nature. “These transactions are not necessarily suitable for countries in severe debt distress, as by that point they would need extensive debt restructuring and relief,” says Patel. “Debt swaps are more suitable for countries with high but not prohibitive debt burdens who want to manage their debt to improve their economic situation.”

Furthermore, donor governments would like to involve private creditors holding developing country debt in these swaps too. However, private lenders are driven by commercial reasoning and will need to be incentivised. One way of achieving that, according to Widge, would be for some of the private creditor debt to be exchanged for validated, high-quality carbon credits that could credibly support private sector net-zero targets. This would also ensure that the swap proceeds are being used by developing economy governments for financing their climate transition efforts.

In fact, to be deployed most effectively, Patel believes the instrument needs to work as part of a suite of debt management and climate and nature financing tools – with, say, any loan agreement building in climate resilient debt clauses as well.

Debt-for-climate swaps could generate $104.5bn for climate and nature

Going forward, debt-for-climate swaps could play an important role in developing countries' decarbonisation agendas. For Ranger, the “sweet spot” for the instrument are nations with relatively high public debt and high mitigation potential; countries with substantial natural resources such as forests and other natural carbon sinks that are also heavily dependent on fossil fuels.

Important as that contribution may be, however, the aggregate impact on the global net-zero transition might still be relatively modest. “It can be a part of the solution to getting to net zero, but – reality check – most of the emissions are coming from countries like the US, China, India, Europe, Japan and Russia,” says Ranger. “And I can't imagine us offering the US or China a debt-for-climate swap any time soon!”

For Steele and Patel, debt-for-climate swaps hold considerable promise. They point to the success of Highly Indebted Poor Countries initiative (HIPC), the Multilateral Debt Relief Initiative (MDRI) and the Brady Plan of the 1980s, 1990s and early 2000s – brought in to deal with the prevailing debt crises across developing countries. Those initiatives demonstrated that for countries in dire straits requiring substantial debt relief, it was still possible to direct some savings from debt relief towards key national development objectives such as poverty reduction projects. Under the HIPC, the net present value of bilateral debt was reduced by 60%; under the MDRI, the net present value of multilateral debt was reduced by 100%; and under the Brady Plan, the value of commercial debt was reduced by 37%.

The IIED did some analysis based on these past initiatives to estimate the amount that could go to climate and nature financing and found that a similar proportion of reductions in the value of bilateral, multilateral and private-sector debt would be instituted again in the current debt crises. The analysis identified 58 countries, holding $497bn in external public and publicly guaranteed debt, that could be part of a climate and nature-related HIPC initiative. It estimated that $397bn could be written off, with 26.3% of that debt relief, $104.5bn, being channelled to climate and nature action. To put that into perspective, that is more than the $100bn annual climate finance goal that developed nations promised – and have consistently failed to deliver – to their developing counterparts as part of the Paris Agreement.

So, the potential and capacity for debt-for-climate swaps to play a fundamental role in global climate action agenda is real – but is the political will?

“These swaps should play a significant role in net zero, but it is not clear to me that they will,” concludes Widge. “Everybody is under the gun: how much appetite is there for Global North governments to prioritise this issue when there are multiple competing priorities – including domestically – that need addressing?”