Swiss-based carbon dioxide removal (CDR) company Climeworks, a global leader in direct air capture (DAC) technology, recently revealed a key shift in geographical focus, announcing its intention to engage in several large-scale DAC projects in the US over the next few years.

Climeworks has applied to participate in three of the US Department of Energy’s (DOE) Regional Direct Air Capture Hubs, collaborating with other CO₂ storage and energy infrastructure organisations and fellow DAC companies. Based in Louisiana, California and the Northern Great Plains, each hub aims to reach a megatonne (one million metric tonnes) of carbon capture capacity by 2030.

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

The company plans to hire more than a hundred employees across the US in the near term, adding to its European workforce of more than 300. By 2030, Climeworks estimates that thousands of direct jobs could emerge from its Regional Direct Air Capture Hubs’ project applications, across project management and operations as well as in construction and manufacturing.

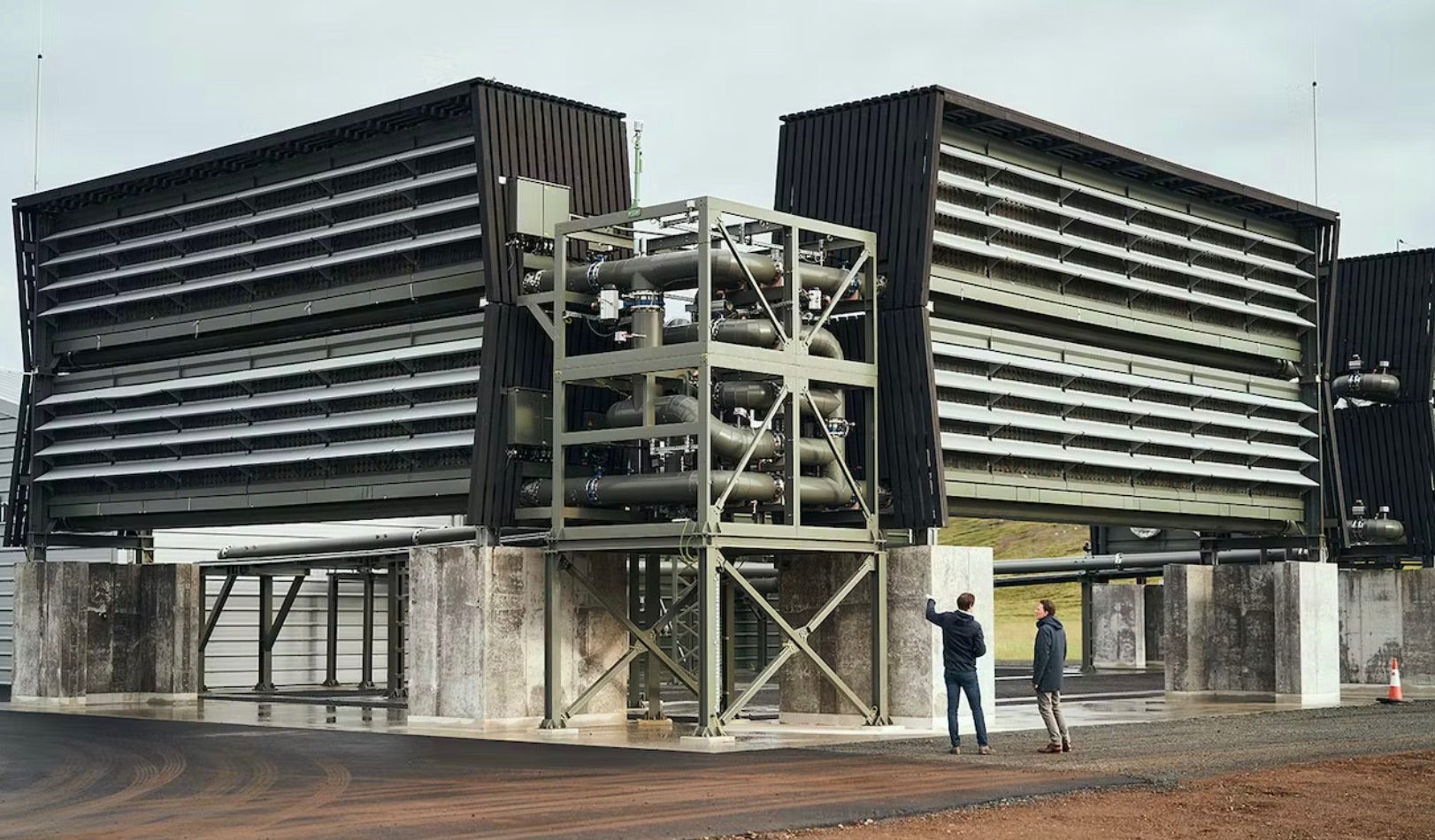

Since its founding in 2009, Climeworks has established the world’s first and, to date, only commercial DAC and storage (DAC+S) plant. ‘Orca’ has been in operation in Iceland since 2021, but the company is currently constructing a new plant, ‘Mammoth‘, which will multiply Orca’s capacity by a factor of nine.

Energy Monitor caught up with Climeworks’ climate policy manager Peter Freudenstein to find out more about the company’s US expansion plans.

Is there any more detail you can share about your US expansion plans? What do your proposals to participate in the three regional DAC hubs consist of?

With the Inflation Reduction Act (IRA) and Infrastructure Investment and Jobs Act, the US has catapulted itself to the very front of global climate action. The support earmarked for carbon dioxide removal via DAC+S makes the US a very attractive market to develop for Climeworks.

In the framework of the DOE’s Regional Direct Air Capture Hubs programme, Climeworks has applied to participate in three hubs with proposed locations in Louisiana, California and the Northern Great Plains – each with a pathway towards megatonne capacity by 2030. It is early days in the process; the DOE is now studying all the applications it has received.

A major focus area for Climeworks in the coming months will be engaging with local communities together with project partners. Fostering constructive and sustained dialogue with stakeholders on topics such as jobs and local environmental protection are key to a successful project.

What does this mean for your European expansion plans? Will the US become Climeworks’ main operational hub in the coming years? How much investment are you planning for each region?

The US is a strategic priority for Climeworks. This is due to unparalleled government funding opportunities and unprecedented political support for DAC as one solution to permanently removing climate-warming CO₂ from the atmosphere. On top of that, many of our pioneering customers, who have understood the role of carbon removal for their company’s net-zero strategies, are based in the US. Add a vibrant ecosystem of storage providers, existing CO2 infrastructure, a skilled workforce, and a home for many leading academic institutions, and you find an attractive place for DAC+S to burgeon into a major industry, creating thousands of jobs.

That being said, the climate problem is global, and so is our ambition to remove a gigatonne [one billion metric tonnes] of CO₂ by 2050. We see increased interest and willingness to support carbon dioxide removal and direct air capture worldwide. We are convinced that the US and its bold leadership only mark the start of global development in that direction.

You say that the US has taken a leadership position in carbon removal. Can you explain the investment incentives it is offering the DAC industry? What does the IRA offer that EU’s Net Zero Industry Act does not?

There are two very concrete incentives now in place in the US that will help accelerate large-scale deployment of DAC: the DOE’s $3.5bn Regional Direct Air Capture Hubs programme and the 45Q tax credit – which also has an improved and specific provision for DAC facilities at $180 per tonne of CO2 stored from them, introduced in the IRA. This represents a big pull for companies like us, as it could provide us with revenue certainty, instil additional investor confidence and thus the means to finance larger-scale facilities. The US is certainly a frontrunner by showcasing strong and concrete commitment to advance DAC and CDR innovation and deployment.

The EU’s Net Zero Industry Act does not include any DAC-specific incentives but sends a very important signal on the need to develop complementary infrastructure such as storage capacity. In addition, the EU does have the Innovation Fund, but it is not yet adapted to the needs of an emerging CDR industry.

Many European cleantech companies have been threatening to move their operations to the US considering the IRA’s attractive investment incentives. What can European policymakers do to stem the tide?

The priority should be defining a clear carbon dioxide removal target in the 2040 target-setting process that is ongoing. Legislators are well-advised to provide planning security and signal to the market that CDR will be needed on a large scale, and soon. On top of that, to help European cleantech developers like Climeworks off the ground, the EU should put in place dedicated CDR policies including unlocking money under the EU Innovation Fund to go toward carbon dioxide removal technologies such as DAC+S.

The EU could take leadership in providing clear signals for a CDR compliance framework starting in the 2030s that could revolutionise a currently largely unregulated voluntary carbon market. Eventually, introducing a subsidy scheme to accelerate CDR deployment in the EU by bringing down its costs is essential in the long run if we want to achieve emission targets globally.

In your announcement, you pointed to the US’s "renewable energy infrastructure and advanced CO₂ storage sites” as appealing reasons for your expansion there. Again, is this something that Europe does not sufficiently offer? Does that mean you will not be partnering with your carbon storage partner for Orca, Carbfix, in the US projects?

Climeworks is exploring storage options throughout the US but also around the world. The US offers several relevant sites and is developing many more for CO₂ storage under the Class VI well-permitting regime. The “readiness” of CO₂ storage sites that follow best practices in reservoir characterisation, monitoring and strict engineering and safety protocols is crucial to the fast deployment of DAC+S.

However, we are also exploring partnerships with other storage providers, such as in Norway and Oman.

After our success with Orca, we are developing our next, larger DAC+S facility, Mammoth, also with Carbfix, and do not exclude further collaboration in the future.

You have previously signed large carbon removal agreements with US corporations such as Microsoft and Boston Consulting Group (BCG). Do you see a larger potential client base in the US than in Europe?

Many of Climeworks’ existing customers are US-based multinationals like Microsoft, Shopify, BCG and Stripe, who have been driving the CDR industry forward with pioneering multi-year offtake agreements. Climeworks hopes to work with many more US companies going forward. Also, we observe decisive action in the US corporate world with many ambitious initiatives for climate action: NextGen, Frontier and various carbon investment funds and other corporate pledges focusing on carbon removal.