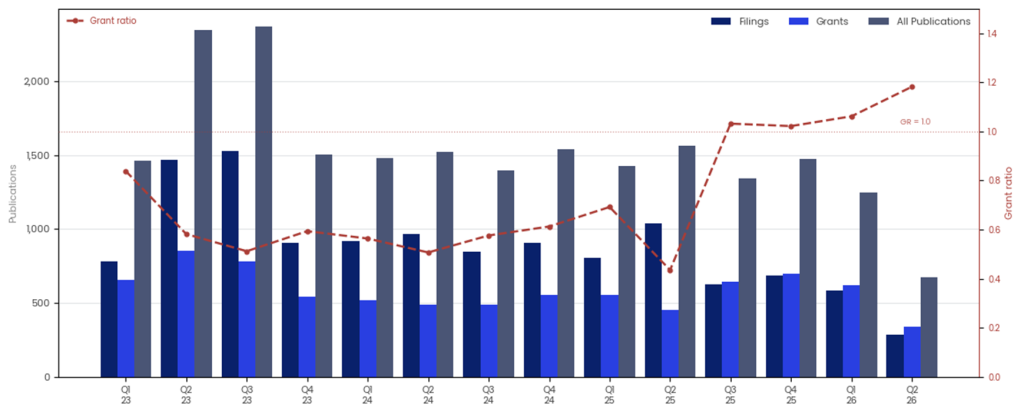

Energy transition patent publications totalled 4,738 in the 12 months to May 2026, a decline of 20.0% from the prior year. Grant ratio (the share of applications that convert to granted patents) rose from 0.570 to 1.057, crossing the 1.0 threshold for the first time in the three-year period. A ratio above 1.0 means prior-period applications are converting to grants faster than new filings arrive. This sector is not retreating. It is resolving.

The IP being granted is higher quality than at any point since 2023

Energy transition patent activity peaked at 2,371 publications in Q3 2023. The TTM quarterly run rate of 1,185 is 50% below that peak. The prior year grant ratio of 0.570 makes the current ratio of 1.057 a near-doubling in conversion quality, a more significant shift than any aggregate volume comparison can convey. For an investor in steel, mining infrastructure, or low-carbon industrial processes, the signal is that the IP positions underpinning commercial operations are being locked in now, while new applications slow. That is a closing window for late entrants and a strengthening moat for those already holding granted estates.

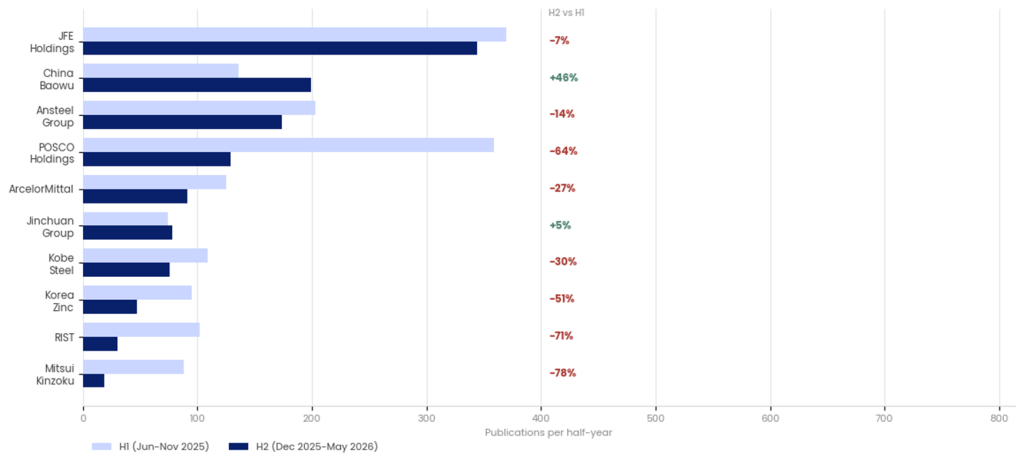

China Baowu Steel Group Corp Ltd (unlisted SOE) accelerated 46.3% in H2 to 199 publications, the strongest momentum in the assignee set. JFE Holdings Inc (TYO: 5411) leads total publications at 714 for the TTM period.

Steel is consolidating, and batteries remain contested. POSCO is caught between

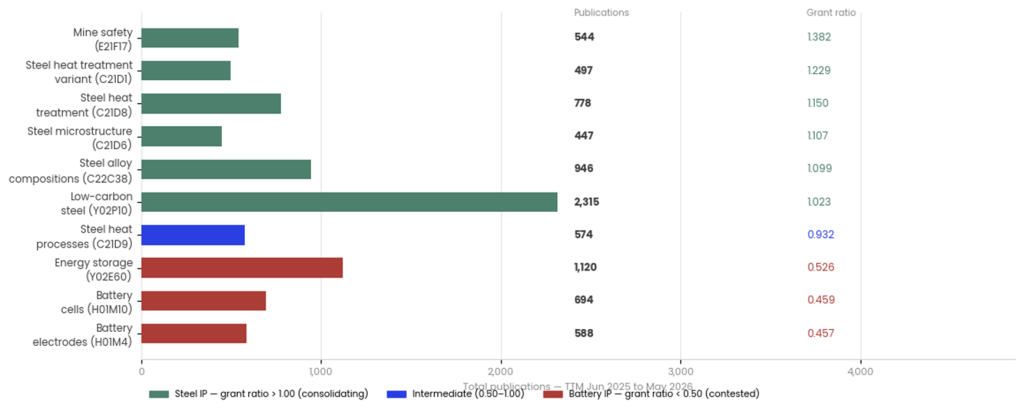

The most analytically revealing dimension of this dataset is the split between steel processing IP, where grant ratios uniformly exceed 1.0, and battery technology IP, where grant ratios sit below 0.46. These are two very different IP races happening simultaneously within the same sector classification.

Low-carbon steel (Y02P10) carries the largest publication volume at 2,315 and converts at 1.023. Steel alloy compositions (C22C38) convert at 1.099. Steel heat treatment processes (C21D8, C21D1, C21D6) convert at 1.150, 1.229, and 1.107 respectively. Mine safety systems (E21F17) convert at 1.382, the highest in the dataset. These are the IP positions that are already formed. Battery cells (H01M10) carry 694 publications at a grant ratio of 0.459. Battery electrodes (H01M4) carry 588 publications at 0.457. Neither has resolved. The battery IP race within energy transition industrials is still open.

POSCO Holdings Inc (KRX: 005490 / NYSE: PKX) is the company that bridges both. Overall, it fell 64.1% in H2 vs H1, the second-largest decline in the dataset. But its concentration in H01M10 battery cell publications, 252 filings in the TTM period, the largest of any named assignee, reveals a strategic pivot from volume steel filings toward battery materials IP. For an investor evaluating POSCO’s transition from steelmaker to battery materials supplier, the patent data makes that repositioning visible before it appears in revenue.

China Baowu is accelerating. RIST has collapsed

Assignee momentum across the TTM period shows one clear accelerator, one significant unreported collapse, and one quiet counter-cyclical grower. China Baowu Steel Group Corp Ltd (unlisted SOE) is the accelerator, up 46.3% in H2. JFE Holdings Inc (TYO: 5411) held broadly, down 7.0% to 344 H2 publications. Ansteel Group Corp Ltd (unlisted SOE) fell 14.3%. ArcelorMittal SA (NYSE: MT / Euronext: MT) fell 27.2%. Kobe Steel Ltd (TYO: 5406) fell 30.3%. Korea Zinc Co Ltd (KRX: 010130) fell 50.5%, and Mitsui Kinzoku Co Ltd (TYO: 5706) fell 78.4%.

The largest decline in the dataset is Research Institute of Industrial Science and Technology (RIST), down 70.6% from H1 to H2, a figure absent from the existing article. RIST is the Korean state-linked research body for steel process development. A fall of this magnitude typically signals programme completion rather than withdrawal, but the pace warrants monitoring across the next TTM period. Jinchuan Group Co Ltd (unlisted SOE) grew 5.4% from H1 to H2, the only named commercial operator besides Baowu posting positive momentum. Its exposure sits primarily in battery materials and non-ferrous metal processing, making it analytically distinct from the steel-dominated assignee set.

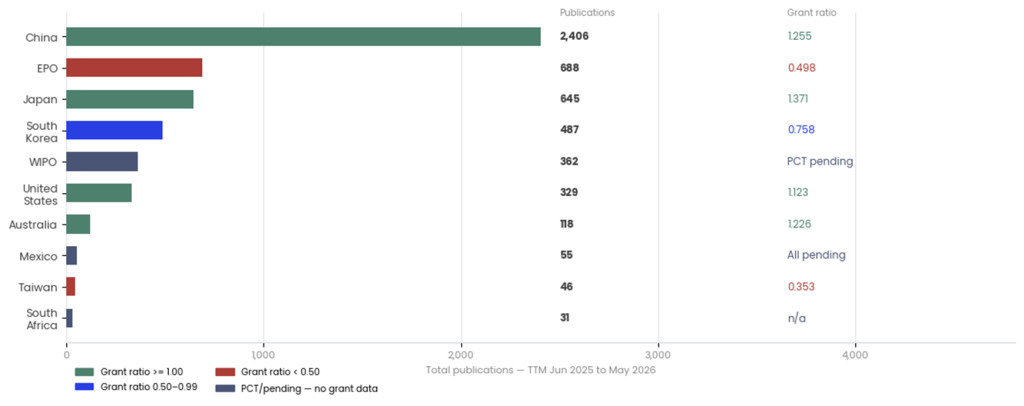

Japan and China convert above 1.0

Japan leads on conversion quality at a grant ratio of 1.371 across 645 publications. China leads by volume at 2,406 publications, 50.8% of the TTM total, at a grant ratio of 1.255. The United States converts at 1.123 across 329 publications. Australia converts at 1.226 across 118 publications.

South Korea sits at 0.758 across 487 publications, the only high-volume jurisdiction below 1.0. Given that POSCO and Korea Zinc are the largest Korean filers and both declined sharply in H2, the 0.758 conversion rate reflects a jurisdiction still in active filing mode on battery materials categories where grants have not yet arrived. The gap between South Korea’s volume (10.3% of TTM) and its conversion rate (0.758 against a sector average of 1.057) is where the battery IP race is most visibly unresolved for an investor with Korean industrials exposure. The European Patent Office converts at 0.498, the only other major authority below the sector average. WIPO carries 362 publications pending national phase entry.

Underground equipment dominates volume

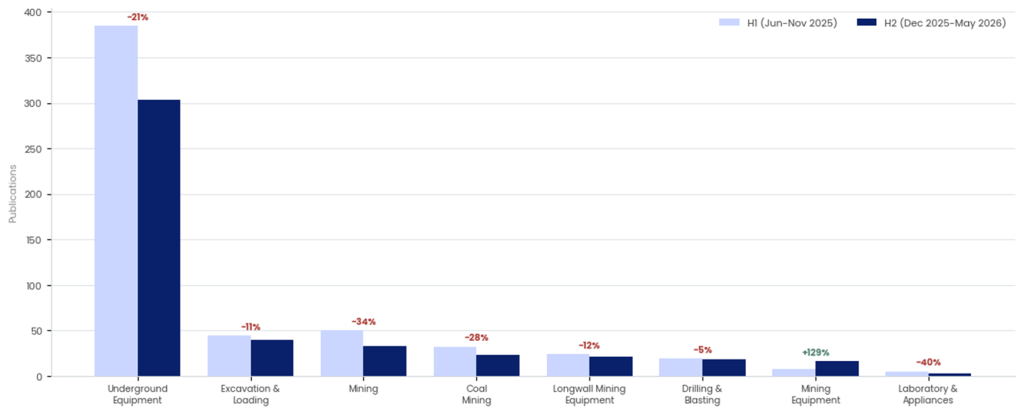

Underground Equipment accounts for 688 TTM publications, the dominant sector by volume, and fell 21.3% from H1 to H2. Coal Mining fell 28.1%, Longwall Mining Equipment fell 12.5%, and Excavation and Loading fell 11.4%. Mining fell 34.0%. The sector-level assignee data shows that the primary filers in Underground Equipment are Chinese academic and state institutions, not listed commercial operators. The volume here reflects state-directed research programme activity rather than commercial IP building.

Mining Equipment grew 128.6%, from 7 publications in H1 to 16 in H2. The absolute numbers are small, but the directional signal is the only positive momentum in a broadly contracting sector universe. For an investor in mining infrastructure equipment, this is the one sub-sector where new IP activity is accelerating within the TTM period.

The evidence that this leads to outperformance

China Baowu and JFE Holdings (TYO: 5411) are building steel IP estates in a period when most peers are retreating. POSCO’s (KRX: 005490 / NYSE: PKX) battery materials pivot is visible in the patent data before it will appear in product revenue. Japan and China are converting applications to grants at rates above 1.0, confirming that the industrial IP positions underlying the energy transition are already forming. The interval between these signals and their appearance in earnings guidance or analyst consensus is where position sizing decisions get made.

Companies identified as innovation leaders through patent indicators show 1.4x higher revenue growth than the broader market. The full evidence for how patent indicators convert into systematic outperformance is set out in GlobalData’s ‘Extracting Innovation Alpha Using Patents’: 5% to 7% annualised alpha over the S&P 500 and 6% to 9% against innovation benchmarks (MSCI World Technology, Nasdaq Composite) across seven years, portfolios outperforming 85% of the time. The energy transition signals in this dataset are one expression of the same underlying dynamic.

Download the free report below or request a data sample by contacting hirendra.vikram@globaldata.com to start translating complex patent activity today.