The Middle East’s energy transition was never going to be linear. The conflict involving Iran has made that unmistakable, after President Trump had already changed the energy landscape. In its early phase, the destruction of fuel depots, industrial sites and urban infrastructure released more than five million tonnes of CO₂ in a matter of weeks, according to an analysis by the Guardian. That is not background noise. It is a surge large enough to offset years of incremental progress in parts of the system.

The Middle East’s formal energy transition continues, but it now unfolds alongside episodes of acute emissions and supply disruption. In effect, it is decarbonising at the margin while absorbing sharp carbon shocks. The result is a transition unfolding in a system that is, at times, quite literally on fire.

Oil retreats at home, but thermal power still dominates

Look past the immediate disruption and the structural direction remains clear. The Middle East is not abandoning hydrocarbons. It is rebalancing how they are used.

Oil and gas still dominate power capacity at roughly 20% and 64%, respectively (as of year-end 2025). In generation terms, the concentration is tighter, with gas producing around 71% of electricity and oil 23%. That is the starting point.

The shift under way is therefore specific. Oil-fired power is being squeezed out because it is emissions-intensive and economically inefficient. Energy Monitor‘s parent company GlobalData expects oil’s share of capacity to fall to around 10% by 2035, with its share of generation dropping to about 11%. Gas remains central, holding roughly 65% of generation even as its capacity share declines more modestly towards 50%.

This is not a move away from thermal power but a reshaping of it. Gas is the only thermal fuel expected to grow in absolute generation over the next decade.

The build pipeline reinforces that point. Between 2026 and 2030, around 86GW of thermal capacity is expected to come online, compared with just 10.8GW of decommissions. In most regions, that would signal backsliding. In the Middle East, it reflects demand growth and the premium placed on reliability.

Saudi Arabia illustrates the logic. It plans to retire roughly 5.9GW of oil-fired capacity by 2030, replacing it with gas and renewables while freeing crude for export. Power sector reform here is as much about export optimisation as it is about emissions.

Solar rises fast, but from a low base

Renewables are expanding quickly, but the starting point matters. Last year, they accounted for just 6% of generation in the region, compared with a global average closer to one third.

That gap explains why the Middle East can build large volumes of solar while still adding thermal capacity. It is not replacing a mature renewable system. It is catching up while meeting rising demand.

By 2035, renewables are forecast to reach around 21% of generation and 38% of capacity. Solar PV does most of the work, rising to roughly 33% of installed capacity and contributing about 18% of generation.

Country trajectories vary widely. Saudi Arabia is expected to lift renewables from around 6% to 38% of generation by 2035. Kuwait is forecast to see solar generation rise from just 93GWh in 2025 to around 21TWh by 2035. Yemen, by contrast, is expected to remain broadly flat at around 704GWh, with conflict continuing to constrain progress.

The economics of solar are no longer the primary barrier – integration is.

Panels in the region operate under extreme conditions, with high temperatures and dust affecting output and maintenance cycles. These factors shape real-world performance and project economics more than headline efficiency gains.

At system level, intermittency is the defining issue. Solar output is concentrated in daylight hours, creating imbalances between supply and demand that must be managed elsewhere in the system.

This brings storage and grid infrastructure into sharper focus.

Storage and grids move to the centre

Energy storage is expanding, but from a low base. Capacity is concentrated in a handful of markets, notably Saudi Arabia, the UAE and Israel.

Saudi Arabia alone is targeting around 48GWh of storage by 2030, with roughly 7GW of rated capacity across active and planned projects. On paper, that suggests momentum. In practice, a significant share remains at the announced or planned stage, where delivery risk is highest.

The physical environment adds complexity. Battery systems must operate in temperatures that can exceed 50°C, raising performance and safety challenges. Developers are therefore prioritising more thermally stable chemistries and investing in cooling systems, increasing both cost and technical demands.

Grids face similar pressure. Expanding transmission capacity and managing variability require sustained investment. Without this layer of infrastructure, renewable capacity cannot translate into reliable supply.

Gas anchors the system, with shifting priorities

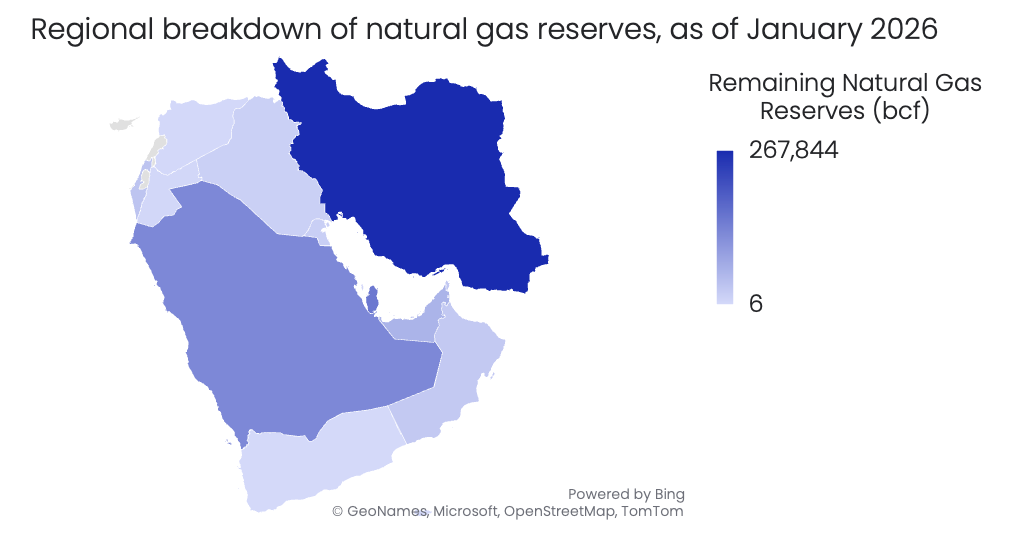

Gas remains the backbone of the power system, supported by substantial regional reserves estimated at around 695,000 billion cubic feet (bcf), with Iran accounting for roughly 270,000bcf.

In 2025, Iran generated approximately 333TWh of gas-fired electricity, the highest in the region. Yet sanctions and geopolitical constraints continue to limit investment and export potential.

More broadly, gas trade dynamics are shifting. Imports have plateaued since 2021, while exports declined in 2025 amid disruption. Events such as temporary shutdowns of offshore fields have highlighted the fragility of supply.

The implication is a gradual rebalancing. Domestic energy security is gaining weight alongside export revenues, particularly in periods of instability.

Emissions shocks complicate the Middle East’s energy transition

The Iran conflict is not just a geopolitical backdrop. It directly affects the region’s emissions profile.

Large-scale fires at fuel storage and industrial sites have released significant volumes of CO₂ and pollutants in short periods. These episodic surges sit alongside longer-term decarbonisation efforts, creating a mismatch between policy trajectories and real-world outcomes.

They also reinforce the value of hydrocarbons in global markets. Supply disruptions push prices higher, strengthening the economic case for continued production and export even as domestic systems shift.

New sectors grow, but constraints persist

Emerging sectors such as sustainable aviation fuel, carbon capture and hydrogen are also gaining traction. The region has around ten active carbon capture, utilisation and storage (CCUS) projects capturing roughly 4.8mtpa, with capacity forecast to approach 30mtpa by 2030.

Hydrogen is expanding rapidly in relative terms, with capacity projected to grow at close to 48% annually through 2030 across roughly 84 projects. However, much of this growth is concentrated in a small number of large developments, raising questions about delivery risk.

Targets are substantial. The Abu Dhabi National Oil Company (ADNOC) aims for 10mtpa of CO₂ capture by 2030, Aramco for 14mtpa by 2035, and Saudi Arabia for 44mtpa. Yet enabling frameworks such as carbon pricing, permitting and incentives remain underdeveloped.

As elsewhere, ambition is easier than execution.

A transition shaped by instability

The overall picture is one of tension rather than contradiction. The Middle East is pursuing a rational reconfiguration of its energy system, reducing reliance on oil in power, expanding gas and scaling renewables.

At the same time, conflict is introducing volatility that affects both emissions and energy markets. Sudden carbon releases, infrastructure damage and supply disruptions sit alongside long-term investment strategies.

Middle East’s energy transition is therefore real, but uneven. It continues, but not in a straight line. The key question is whether the supporting systems, physical, regulatory and political, can evolve quickly enough to keep it on track.

This article is derived from and informed by a GlobalData report. All data, forecasts and project metrics are sourced from that GlobalData extract unless otherwise indicated.

To access the full report, visit the GlobalData Power Intelligence Centre: www.globaldata.com/industries/power.